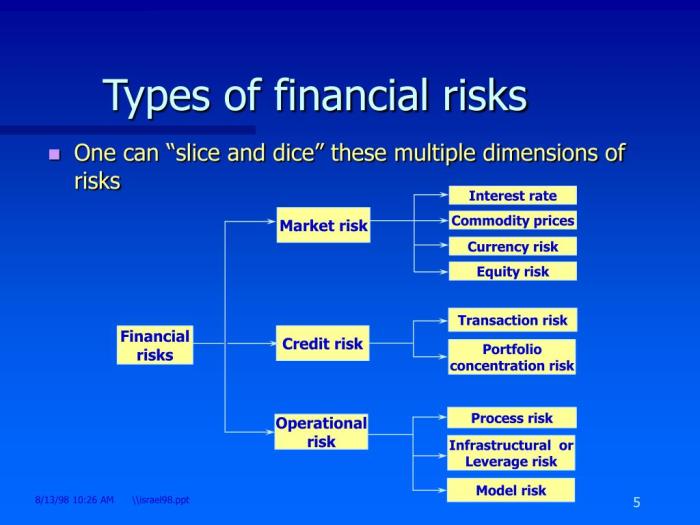

Understanding credit risk is paramount in the financial world, impacting lenders, borrowers, and investors alike. From individual credit card applications to large-scale corporate loans, the potential for loss due to borrower default or other unforeseen circumstances is ever-present. This exploration delves into the various types of credit risk, examining their nuances and implications for effective risk management.

This analysis will dissect different credit risk categories, highlighting the distinctions between default risk and other forms, such as concentration risk and prepayment risk. We will explore the role of credit scores, regulatory frameworks, and technological advancements in shaping credit risk assessment and mitigation strategies. By understanding these complexities, we can better navigate the challenges and opportunities within the credit landscape.

Mitigation Strategies for Credit Risk

Financial institutions face significant challenges in managing credit risk, the potential for losses stemming from borrowers’ failure to repay their obligations. Effective mitigation strategies are crucial for maintaining financial stability and profitability. These strategies aim to minimize the likelihood and impact of defaults, ensuring the long-term health of the institution.

A robust approach to credit risk mitigation involves a combination of proactive measures and reactive responses. Institutions employ various techniques, often in concert, to manage their exposure to credit losses.

Credit Risk Mitigation Strategies

Financial institutions utilize a diverse range of strategies to effectively manage credit risk. These strategies work together to create a comprehensive risk management framework. The selection and implementation of these strategies depend heavily on the specific nature of the credit risk, the institution’s risk appetite, and the overall economic environment.

- Diversification: Spreading credit exposure across a wide range of borrowers and industries reduces the impact of defaults by individual borrowers. This strategy minimizes the concentration of risk within a portfolio.

- Credit Scoring and Analysis: Rigorous assessment of borrowers’ creditworthiness through detailed financial analysis, credit scoring models, and background checks helps identify potentially risky borrowers early in the lending process.

- Collateralization: Requiring collateral, such as real estate or other assets, as security for loans reduces lender losses in the event of default. The collateral can be liquidated to recover some or all of the outstanding loan amount.

- Loan Covenants: Incorporating restrictive covenants into loan agreements imposes conditions on borrowers, such as maintaining certain financial ratios or refraining from specific actions, to protect the lender’s interests.

- Stress Testing and Scenario Analysis: Simulating various economic scenarios, including adverse conditions, allows institutions to assess the potential impact of credit losses on their portfolios and adjust their risk management strategies accordingly.

- Provisioning for Loan Losses: Setting aside reserves to cover potential loan losses allows institutions to absorb unexpected defaults without significantly impacting their financial health. These provisions are based on historical data and credit risk assessments.

- Early Warning Systems: Implementing systems that monitor borrowers’ financial performance and identify early signs of potential default enables proactive intervention and potentially prevents larger losses.

The Importance of Diversification in Managing Credit Risk Portfolios

Diversification is a cornerstone of effective credit risk management. By spreading credit exposure across a wide range of borrowers and industries, financial institutions significantly reduce the impact of defaults. If a single borrower or industry experiences financial distress, the overall impact on the portfolio is lessened. This reduces the likelihood of a significant portfolio-wide loss. For example, a bank lending to multiple industries (e.g., technology, healthcare, manufacturing) is less vulnerable than a bank solely focused on the real estate sector during a real estate market downturn.

Credit Derivatives and Risk Transfer Mechanisms

Credit derivatives and other risk transfer mechanisms provide institutions with tools to actively manage and reduce their credit risk exposure. These instruments allow institutions to transfer some or all of their credit risk to other parties.

- Credit Default Swaps (CDS): These are contracts where one party pays a premium to another in exchange for protection against a specific borrower’s default. The buyer of the CDS receives a payment from the seller if the borrower defaults.

- Collateralized Debt Obligations (CDOs): These are structured financial products that pool together various debt instruments, such as mortgages or corporate bonds, and then repackage them into tranches with varying levels of risk and return.

While these instruments can be effective risk management tools, they also carry their own complexities and risks. The 2008 financial crisis highlighted the dangers of excessive reliance on complex credit derivatives and the need for careful oversight and regulation.

Comparison of Credit Risk Mitigation Techniques

The effectiveness and cost of different credit risk mitigation techniques vary significantly. For instance, diversification is generally a cost-effective strategy, while credit derivatives can be expensive but offer more targeted risk reduction. Credit scoring and analysis are relatively low-cost preventative measures, whereas provisioning for loan losses requires capital allocation and potentially reduces profitability in the short term. The optimal approach involves a tailored combination of techniques that balances cost and effectiveness based on the institution’s specific circumstances and risk appetite.

For example, a smaller bank might rely more heavily on diversification and careful credit analysis, while a larger, more complex institution might utilize a wider array of tools, including credit derivatives and sophisticated risk models.

Credit Risk and Regulatory Frameworks

The financial stability of nations hinges significantly on robust credit risk management. Regulations play a crucial role in ensuring that financial institutions adequately assess, manage, and mitigate credit risk, protecting both the institutions themselves and the broader economy. These frameworks evolve in response to past crises and emerging challenges, constantly striving for improved risk management practices.Regulatory bodies worldwide have established a complex web of rules and guidelines aimed at reducing the likelihood and impact of credit-related failures.

These regulations impact lending practices, credit assessment methodologies, and the overall stability of the financial system. Understanding these frameworks is critical for both financial institutions and policymakers.

Key Regulations for Credit Risk Management

Numerous regulations aim to control and mitigate credit risk. These vary in detail depending on the jurisdiction and the type of financial institution, but common themes include capital requirements, stress testing, and disclosure requirements. For instance, Basel Accords, a set of international banking regulations, set minimum capital requirements for banks based on their risk profile. These requirements ensure banks have sufficient capital to absorb potential losses from credit defaults.

Similarly, Dodd-Frank Act in the US, implemented after the 2008 financial crisis, introduced stricter regulations for financial institutions, including increased capital requirements and enhanced oversight.

The Role of Regulatory Bodies in Overseeing Credit Risk Management

Regulatory bodies, such as the Federal Reserve in the US, the European Central Bank (ECB), and national banking authorities globally, play a vital role in overseeing credit risk management practices. Their responsibilities include setting and enforcing regulations, conducting regular inspections and audits of financial institutions, and monitoring the overall health of the financial system. They use a combination of quantitative and qualitative assessments to evaluate the effectiveness of credit risk management systems.

This oversight aims to prevent excessive risk-taking and maintain the stability of the financial system. These bodies also frequently publish reports and guidance to help institutions improve their credit risk management practices.

Impact of Regulatory Changes on Lending Practices and Credit Risk Assessment

Regulatory changes can significantly influence lending practices and credit risk assessment methodologies. For example, stricter capital requirements might lead to a reduction in lending, particularly to riskier borrowers. Changes in disclosure requirements can increase transparency and improve market discipline. The implementation of new stress testing methodologies forces institutions to better understand and manage their exposure to various economic scenarios.

These changes often lead to more conservative lending practices and a more rigorous approach to credit risk assessment.

Examples of Regulatory Failures and Their Consequences

The failure to adequately regulate the financial industry can have devastating consequences, as seen in the 2008 global financial crisis. Inadequate oversight of subprime mortgages, coupled with lax lending standards and a lack of transparency, led to a widespread collapse in the housing market and a global recession. This highlighted the critical importance of effective regulation and supervision in preventing systemic risk.

Other examples include regulatory failures related to the savings and loan crisis in the US in the 1980s and various banking crises around the world. These failures often result in significant economic losses, financial instability, and damage to public trust.

Impact of Technology on Credit Risk Management

Technological advancements are revolutionizing credit risk management, offering unprecedented opportunities to enhance accuracy, efficiency, and overall effectiveness. The integration of big data analytics, artificial intelligence (AI), and machine learning (ML) is transforming how financial institutions assess and manage credit risk, leading to both significant benefits and new challenges.The application of technology is fundamentally altering credit risk assessment. Traditional methods often relied heavily on limited data points and manual processes, leading to potential biases and inaccuracies.

Modern techniques, however, leverage vast datasets to create more comprehensive and nuanced risk profiles. This allows for a more granular understanding of borrower behavior and the identification of subtle indicators of potential default.

Big Data Analytics and AI in Credit Risk Assessment

Big data analytics allows credit lenders to process and analyze massive datasets encompassing various sources, including traditional credit reports, social media activity, online purchase history, and even geolocation data. AI algorithms can then identify complex patterns and correlations within these datasets that would be impossible for humans to detect manually. This leads to more accurate credit scoring models, better prediction of default probabilities, and improved risk stratification.

For instance, a lender might use AI to identify a borrower with a seemingly good credit score but a history of high-risk online transactions, prompting a more thorough review of their application. The result is a more precise and objective assessment of creditworthiness.

Technological Applications in Fraud Detection and Prevention

Technology plays a critical role in detecting and preventing credit fraud. AI-powered systems can analyze transaction data in real-time, identifying anomalies and suspicious patterns indicative of fraudulent activity. These systems can flag potentially fraudulent transactions for human review or even automatically block them, minimizing financial losses. For example, a system might detect a sudden surge in transactions from an unusual location or a significant increase in spending compared to a borrower’s typical behavior, triggering an alert.

Biometric authentication methods, such as fingerprint or facial recognition, further enhance security and reduce the risk of unauthorized access to accounts. Advanced machine learning models continuously learn and adapt, improving their accuracy in detecting new and evolving fraud schemes.

Benefits and Challenges of Technology in Credit Risk Management

The benefits of using technology in credit risk management are substantial. Improved accuracy in credit scoring leads to better lending decisions, reducing both defaults and missed opportunities. Automated processes increase efficiency, reducing operational costs and freeing up human resources for more strategic tasks. Enhanced fraud detection capabilities minimize financial losses and protect the integrity of the financial system.However, challenges remain.

The reliance on complex algorithms raises concerns about transparency and explainability. It can be difficult to understand why a particular credit decision was made, potentially leading to disputes and regulatory scrutiny. Data privacy and security are paramount; the use of vast datasets necessitates robust security measures to prevent data breaches and protect sensitive customer information. The cost of implementing and maintaining sophisticated technology can be significant, potentially creating a barrier for smaller institutions.

Finally, the potential for algorithmic bias, where algorithms perpetuate existing societal biases, must be carefully addressed.

Scenario: Enhanced Credit Risk Management with Predictive Modeling

Imagine a new technological advancement: a predictive model that incorporates real-time economic indicators and social sentiment analysis alongside traditional credit data. This model could anticipate shifts in the economic climate and their impact on borrower behavior. For example, if the model detects a significant increase in unemployment claims and negative social media sentiment related to financial hardship, it could proactively adjust credit risk assessments and lending policies, reducing potential losses during economic downturns.

This proactive approach, powered by advanced predictive analytics, would represent a significant improvement in credit risk management, allowing lenders to adapt to changing circumstances and mitigate risk more effectively.

In conclusion, navigating the multifaceted landscape of credit risk requires a comprehensive understanding of its various forms and the tools available for mitigation. While technology offers innovative solutions for assessment and fraud prevention, a robust framework of regulatory oversight and diversification remains crucial. By proactively addressing these challenges, financial institutions and individuals can effectively manage their exposure to credit risk and foster a more stable and resilient financial ecosystem.

Commonly Asked Questions

What is the difference between secured and unsecured credit?

Secured credit involves collateral (e.g., a house for a mortgage), limiting lender loss in case of default. Unsecured credit, like credit cards, has no collateral, making it riskier for lenders.

How can macroeconomic factors influence credit risk?

Economic downturns increase unemployment and reduce income, leading to higher default rates. Inflation can erode the value of loan repayments, also impacting credit risk.

What are some examples of credit risk mitigation strategies beyond diversification?

Stress testing, setting aside reserves, and using credit derivatives to transfer risk are additional mitigation techniques.

How does AI impact credit risk assessment?

AI algorithms can analyze vast datasets to identify patterns and predict defaults more accurately than traditional methods, improving credit scoring and fraud detection.